Last updated: January 2026 to reflect current Thai gift tax rules and Revenue Department practice.

Thailand does have a gift tax, but it applies far more narrowly than many expats expect.

In practice, gift tax is aimed at large, deliberate transfers of wealth, not at everyday financial support between family members. Most expats living in Thailand will never pay gift tax. Where people run into problems is usually not because of the tax itself, but because a transfer is poorly structured, poorly documented, or misunderstood.

This guide explains how gift tax works in practice for expats in Thailand. It sets out when gift tax can apply, the current thresholds and rates, how the rules are typically interpreted, and where caution is needed. The focus is on real-world situations rather than theory, so you can understand whether the rules are relevant to you and how to manage risk sensibly.

Key Definitions Used in This Guide

The following terms are used consistently throughout this article. These definitions reflect how the concepts are commonly applied under Thai tax law and practice.

Gift: A transfer of money or assets from one person to another where the recipient gives nothing, or less than market value, in return.

Gift tax: A form of personal income tax that may apply when the value of gifts received by an individual exceeds certain annual thresholds.

Gift with reservation: A situation where something is described as a gift, but the giver continues to benefit from the asset or funds. While this is not a formal Thai legal term, it reflects the Revenue Department’s substance-over-form approach and is not treated as a genuine gift for tax purposes.

Tax resident (Thailand): An individual who spends 180 days or more in Thailand in a calendar year. Tax residency affects how income and certain transfers are treated when money is brought into Thailand.

Remittance: The act of transferring money into Thailand, typically from an overseas account. For tax residents, the timing and nature of remittances can be relevant.

Ascendant/Descendant: Ascendants include parents and grandparents. Descendants include children and grandchildren.

Market value: The price an asset would reasonably achieve in an open market between unrelated parties.

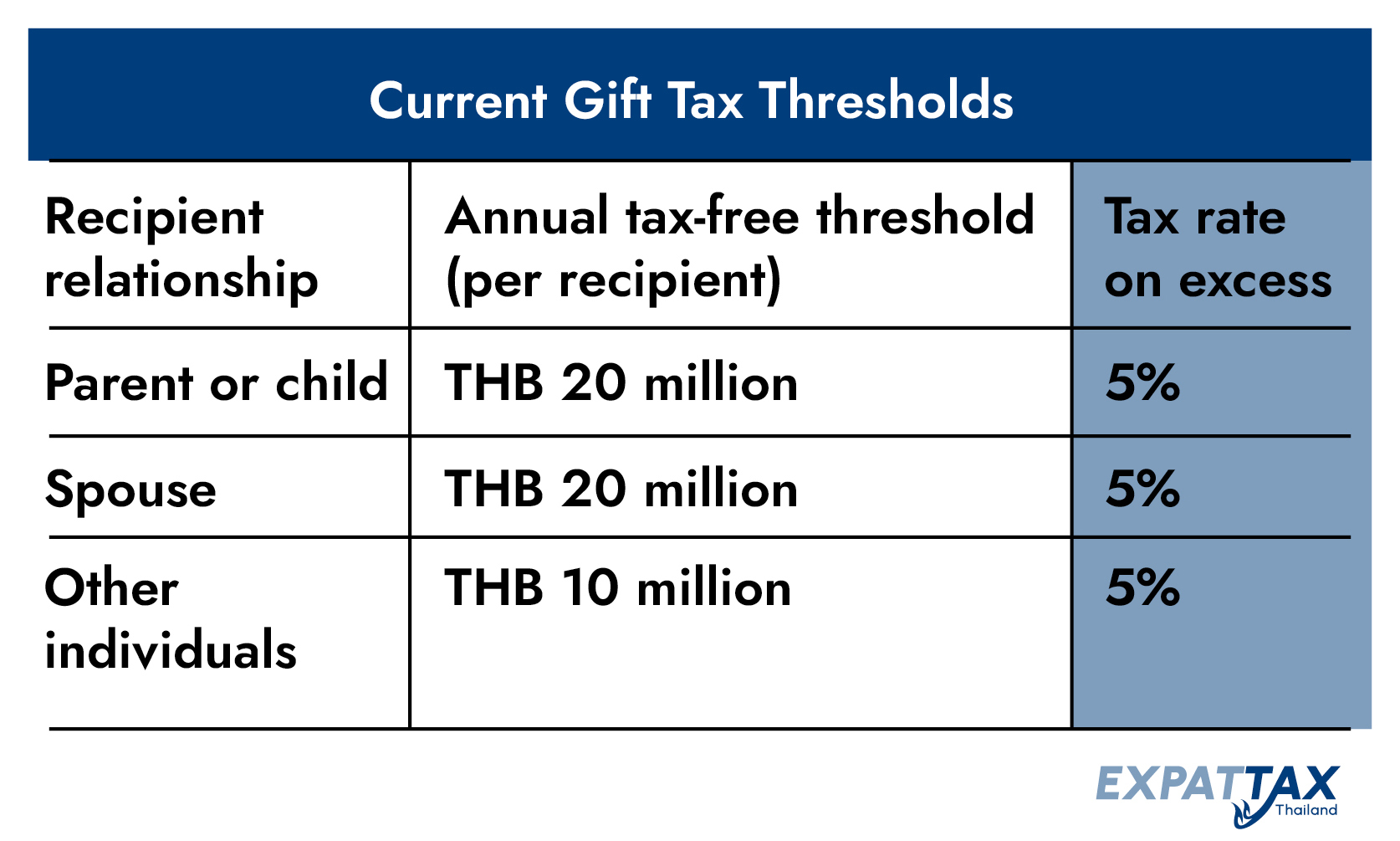

Gift Tax Thresholds and Rates in Thailand

Gift tax in Thailand is based on who the recipient is and the total value of gifts received in a tax year. The tax is assessed on the recipient, not the giver.

Key points to note:

- Thresholds apply per recipient per calendar year

- Multiple gifts in the same year are assessed cumulatively

- Only the amount above the threshold is subject to tax

- In many cases, a 5% rate applies once the threshold is exceeded

For most cash gifts and many family gifts, tax is calculated at 5% on the amount above the threshold. For some transfers of immovable property, particularly outside the immediate family exemptions, withholding may be applied at progressive personal income tax rates at the time of registration.

These thresholds mean that gift tax generally becomes relevant only for large, intentional transfers, rather than routine financial support or day-to-day living costs.

Gifts vs Living Expenses: Why Most Family Support Is Not Taxable

One of the most common areas of confusion for expats in Thailand is the difference between a taxable gift and ordinary financial support.

In practice, Thai gift tax is not aimed at day-to-day family support. It is designed to apply to large, deliberate transfers of wealth, where ownership and benefit are clearly passed from one person to another.

Living Expenses Are Usually Not Treated as Gifts

Regular financial support that covers ordinary living costs is generally not treated as a taxable gift, even when money is transferred between family members.

Examples commonly seen in practice include:

- Monthly transfers to a spouse to cover household expenses

- Money used for rent, utilities, food, education or healthcare

- Shared access to funds used for family living costs

- Support paid from overseas to meet ongoing personal expenses in Thailand

In these situations, the money is typically consumed as part of daily living, rather than transferred as an asset that the recipient can freely retain or invest. For this reason, such payments are not usually viewed as gifts for gift tax purposes.

When Financial Support Can Become a Taxable Gift

A transfer that looks like family support can begin to resemble a taxable gift if it involves:

- Large one-off lump sums

- Funds transferred without a clear spending purpose

- Money that is retained, invested, or accumulated by the recipient

- Transfers that exceed the relevant annual gift tax thresholds

For example, sending a substantial lump sum to a family member, which is then saved or invested in their own name, may be treated differently from regular support used for living costs.

The key question in practice is whether the transfer represents a genuine shift of wealth, rather than ongoing support.

Gifts With Reservation: Where Problems Arise

A critical concept in Thai gift tax is the ‘gift with reservation’.

A gift with reservation occurs where something is described as a gift, but the original owner continues to benefit from it in some way. In these cases, the transfer may not be recognised as a genuine gift for tax purposes.

Common examples include:

- Money transferred to a spouse but still used to pay the giver’s own expenses

- Assets placed in another person’s name while control or benefit is retained

- Funds moved temporarily to avoid tax and later returned or reused

Where a gift with reservation exists, the Revenue Department may disregard the gift treatment altogether and assess the transaction based on its substance rather than its label.

Practical Guidance for Expats

To reduce uncertainty and avoid unintended risk:

- Keep everyday support separate from large one-off transfers

- Be clear about the purpose of significant payments

- Avoid describing living expenses as ‘gifts’ unnecessarily

- Seek advice before making large transfers intended as gifts

Most expats who are simply supporting their household or family members do not need to worry about gift tax. Issues tend to arise only where transfers are large, poorly documented, or structured in a way that does not reflect how the money is actually used.

Gift Tax Rules for Expats and Foreigners

How gift tax applies in Thailand depends heavily on tax residency and the nature of the assets involved. For expatriates, misunderstandings often arise because gift tax is confused with income tax or remittance rules. In practice, the interaction is narrower and more specific.

Expatriates Who Are Thai Tax Residents

An expat who is a Thai tax resident is someone who spends 180 days or more in Thailand in a calendar year.

For tax residents:

- Gift tax may apply when they receive gifts that exceed the annual thresholds

- The tax is assessed on the recipient, not the giver

- The location of the giver does not, by itself, determine tax treatment

Gift tax is separate from income tax. A gift is not taxed because it is foreign or domestic, but because it exceeds the relevant gift tax threshold and meets the definition of a genuine gift.

Where confusion often arises is when gifts are remitted into Thailand. While remittance timing can matter for income tax, gift tax focuses primarily on the nature and value of the transfer, rather than the timing alone.

Expatriates Who Are Not Thai Tax Residents

Expats who do not meet the 180-day threshold are generally taxed in Thailand only on Thai-sourced income.

However, gift tax can still be relevant in certain situations, particularly where the gift involves:

- Thai real estate

- Shares in Thai companies

- Other assets located in Thailand

In these cases, gift tax may apply regardless of the giver’s residency status, because the asset itself is connected to Thailand.

Gifts Received from Overseas

Receiving a gift from outside Thailand does not automatically make it taxable.

What matters in practice is:

- Whether the transfer meets the definition of a genuine gift

- Whether the annual gift tax thresholds are exceeded

- Whether the transfer represents a real shift of ownership

Many overseas family transfers fall well below the thresholds and never trigger gift tax. Larger transfers, particularly one-off amounts intended to be retained or invested, require more careful consideration.

Overseas Gifts and Remittances

If you are a Thai tax resident, foreign-sourced assessable income may be subject to Thai tax when remitted into Thailand. Whether an overseas transfer is treated as a gift, support, or another category depends on the facts, the relationship, and the evidence. For large overseas transfers, it is sensible to document purpose and structure clearly before remitting funds into Thailand.

The Role of Documentation

For expatriates, documentation is often more important than the tax itself.

Clear records help demonstrate:

- Who gave the funds

- Why they were transferred

- Whether they were intended as support or as a gift

- How the funds were ultimately used

Poor documentation is one of the most common reasons otherwise straightforward family transfers become problematic.

Key Takeaway for Expats

Gift tax in Thailand is not triggered simply because someone is foreign, nor because money comes from overseas. It becomes relevant only when a transfer:

- Qualifies as a genuine gift

- Exceeds the applicable thresholds

- Represents a true transfer of wealth

For most expats, everyday family support remains outside the scope of gift tax. Issues tend to arise only where transfers are large, poorly structured, or inconsistent with how the money is actually used.

Common Expat Scenarios: How Gift Tax Applies in Practice

This section looks at the situations most commonly encountered by expats in Thailand and explains how gift tax is typically approached in each case. These examples are illustrative rather than exhaustive, but they reflect how the rules are commonly applied in practice.

Gifts to a Thai Spouse

Transfers between spouses are one of the most common areas of concern, and also one of the most misunderstood.

Gifts between spouses benefit from a higher annual tax-free threshold, currently THB 20 million per recipient. This means that even substantial transfers will often fall outside the scope of gift tax.

However, the way the money is used still matters. Regular transfers to cover household costs or shared living expenses are generally treated as ordinary support rather than gifts. Larger lump sums that are retained, saved, or invested in the spouse’s own name are more likely to be viewed as genuine gifts.

Problems tend to arise when funds are described as a gift but are used primarily for the giver’s own benefit. In such cases, the arrangement may be treated as a gift with reservation rather than a genuine transfer of wealth.

Parents Supporting Children in Thailand

Parents often send money to support children studying or living in Thailand.

Where funds are used for education, accommodation, or general living costs, they are typically treated as support payments, not taxable gifts. This is particularly true where transfers are regular and linked to identifiable expenses.

Larger one-off transfers, such as money given to help purchase property or establish a business, may fall within the gift tax framework if they exceed the relevant annual threshold. In these cases, documentation and clarity of purpose become important.

Children Supporting Parents or Other Ascendants

Financial support flowing upwards within a family is less common but still relevant.

Regular support for living or medical expenses is generally not treated as a taxable gift. Where a significant asset or lump sum is transferred outright, gift tax may become relevant, subject to the higher threshold that applies to ascendants.

As with other scenarios, the distinction lies in whether the transfer represents ongoing support or a permanent transfer of wealth.

Family Sending Money from Overseas

Many expats receive money from family members outside Thailand.

Receiving funds from overseas does not, by itself, trigger gift tax. What matters is:

- The total value received in a tax year

- Whether the funds are genuinely gifted

- Whether they are retained or accumulated

Smaller or irregular transfers for support purposes rarely raise issues. Large one-off transfers intended to be kept or invested require more careful planning, particularly where the recipient is a Thai tax resident.

Large One-Off Transfers

Large lump sums attract the most scrutiny and are where gift tax is most likely to apply.

Examples include:

- Money transferred to assist with property purchases

- Capital provided to start or expand a business

- Significant cash gifts intended as part of long-term estate planning

In these cases, it is important to consider the annual thresholds, the relationship between the parties, and whether the transfer should be spread over multiple years or structured differently.

Gifting Assets Before Death vs Inheritance

Some expats consider gifting assets during their lifetime rather than passing them on through inheritance.

Gift tax and inheritance tax are separate regimes in Thailand, with different thresholds and conditions. Lifetime gifts may reduce exposure to inheritance tax, but they must still be assessed under the gift tax rules at the time they are made.

This type of planning requires careful coordination, particularly where assets or family members are spread across multiple countries.

Practical Observation

Across all scenarios, the same themes recur:

- Ordinary family support is rarely the issue

- Large, poorly explained transfers create risk

- Substance matters more than labels

Understanding how these principles apply to your own circumstances is usually more important than the headline tax rates themselves.

Gift Tax and Double Taxation: How International Rules Interact

For expats, gift tax rarely exists in isolation. Many gifts involve people, assets, or bank accounts in more than one country, which raises understandable concerns about double taxation.

In practice, managing this risk requires an understanding of both Thai tax rules and the tax treatment of gifts in the other country involved.

Do Double Tax Agreements Cover Gift Tax?

Thailand has entered into double tax agreements (DTAs) with many countries. These agreements are primarily designed to prevent the same income from being taxed twice.

Most DTAs do not explicitly cover gift tax.

This means that, in many cases, gift tax is dealt with under each country’s domestic law rather than resolved through a treaty mechanism. Where relief is available, it is usually indirect rather than automatic.

How Double Taxation Can Arise in Practice

Double taxation issues are most likely to arise where:

- The giver and recipient are in different countries

- The country of the giver applies gift or inheritance tax rules

- The recipient is a Thai tax resident and receives a large gift

For example, some countries focus on taxing the giver, while Thailand taxes the recipient. This difference in approach can create overlapping exposure if not planned carefully.

Common Cross-Border Considerations

Gifts From the UK

The UK does not tax the recipient of a gift. Instead, gifts are treated as potentially exempt transfers for inheritance tax purposes. If the giver dies within seven years of making the gift, inheritance tax may become payable.

A gift received in Thailand may still fall within Thai gift tax rules if the thresholds are exceeded, even though the UK does not charge gift tax at the time of transfer.

Gifts From the United States

The US applies gift tax primarily to the giver, subject to annual exclusions and lifetime exemptions. In many cases, no immediate US tax is payable.

However, a large gift received by a Thai tax resident may still be subject to assessment under Thailand’s gift tax framework, as the two systems operate independently.

Gifts From Europe and Other Countries

Approaches vary widely across Europe and elsewhere. Some countries tax gifts heavily, others barely at all. The absence of treaty coverage requires careful coordination when substantial transfers are involved.

Practical Risk Management

Gift tax rules differ by country and as a result are not always aligned:

- Do not assume a gift that is tax-free abroad is automatically tax-free in Thailand

- Do not assume treaty relief applies unless it clearly does

- Consider both giver-side and recipient-side exposure

For larger transfers, it is usually sensible to obtain advice that considers both jurisdictions together, rather than reviewing Thai tax in isolation.

Key Takeaway

Double taxation issues around gifts are less about aggressive enforcement and more about mismatched systems. The risk is usually manageable, but only if the rules in each country are understood and coordinated properly.

How Gift Tax Is Declared in Practice

Gift tax in Thailand is not declared through a separate standalone filing. Instead, it is handled as part of the personal income tax return process. This is one reason it is often overlooked or misunderstood.

When Gift Tax Is Reported

Gift tax is assessed in the tax year in which the gift is received.

For individuals, this means it is declared as part of the annual personal income tax filing, which follows the calendar year. If a gift is received during the year and exceeds the relevant threshold, it should be assessed and reported in that year’s return.

There is no advance approval process for gift tax. It operates on a self-assessment basis, relying on the taxpayer to assess whether the thresholds have been exceeded and to declare the tax correctly.

How Gift Tax Appears on the Tax Return

Gift tax is declared using the standard Personal Income Tax Return (PND.90).

In practice:

- The value of the taxable portion of the gift is included as assessable income

- The specific gift tax rate is applied to the excess over the threshold

- Supporting documentation is retained rather than routinely submitted

The Revenue Department does not require a special gift tax form. This reinforces the importance of understanding how gifts are classified and recorded, particularly where large transfers are involved.

Documentation Typically Expected

Although documentation is not always requested at the time of filing, taxpayers should be able to demonstrate:

- The source of the funds or asset

- The relationship between the giver and the recipient

- The date the gift was received

- The value of the gift

- How the funds or asset were intended to be used

For larger gifts, a written gift agreement can help clarify intent, particularly when the transfer might otherwise be confused with income or support payments.

Common Filing Mistakes

Most issues arise not because gift tax is inherently complex, but because it is misclassified or ignored.

Common mistakes include:

- Treating large gifts as living expenses without evidence

- Failing to aggregate multiple gifts received in the same year

- Under-valuing non-cash assets

- Assuming overseas gifts never need to be considered

- Declaring gifts inconsistently with how funds are actually used

These mistakes are usually the result of misunderstanding rather than deliberate non-compliance.

What Happens If a Gift Is Identified Later?

If a taxable gift is identified after a return has been filed, it can usually be addressed through an amended return.

Where the issue arises from poor documentation or misclassification, the focus is typically on correcting the tax position rather than imposing punitive measures. As with other areas of Thai tax, clarity and cooperation tend to matter more than rigid formalities.

Practical Takeaway

Gift tax compliance in Thailand is largely about classification and record-keeping, not complex filings or aggressive enforcement.

Expats who:

- Understand the thresholds

- Keep clear records

- Separate everyday support from genuine gifts

are unlikely to encounter difficulties.

Record-Keeping and Evidence: What the Revenue Department Expects

In most gift tax cases, the deciding factor is not the tax rate, but the quality of the records. Clear documentation helps demonstrate whether a transfer was ordinary support or a genuine gift and whether gift tax thresholds were exceeded.

The Thai Revenue Department does not prescribe a single formal document for gifts. Instead, it expects taxpayers to be able to explain and evidence the nature of significant transfers if asked.

Records Commonly Expected in Practice

For gifts that may fall within the gift tax framework, it is sensible to retain:

- Bank statements showing the transfer of funds

- Dates on which the funds or assets were received

- Evidence of the relationship between the giver and recipient

- The purpose of the transfer, where relevant

- Valuations for non-cash assets, such as property or shares

These records help establish both intent and value, which are the two central questions in gift tax assessments.

Written Gift Agreements

For larger gifts, a simple written agreement can be useful.

A gift agreement typically sets out:

- Who is giving the gift

- Who is receiving it

- What is being transferred

- The date of transfer

- Confirmation that no benefit is retained by the giver

While not legally required in every case, such agreements can help avoid later confusion, particularly where the transfer could otherwise be mistaken for income, a loan, or temporary support.

Tracking Gifts Over Time

Gift tax thresholds are assessed on an annual cumulative basis.

This means it is important to:

- Track multiple gifts received from the same person in the same year

- Keep year-by-year records rather than relying on account balances

- Avoid mixing large gifts with routine living expense transfers

Clear separation makes it easier to demonstrate whether thresholds have been exceeded and reduces the risk of misclassification.

Interaction With Banking and AML Checks

Banks may ask questions about the source and purpose of significant transfers as part of their anti-money laundering obligations.

These enquiries are separate from tax assessments, but consistent documentation helps ensure that explanations given to banks and those reflected in tax filings do not conflict.

Practical Takeaway

For gift tax purposes, the goal of record-keeping is not perfection. It is clarity.

Expats who can clearly show:

- Where money came from

- Why it was transferred

- How it was used

are generally well placed to address any questions that arise.

Myths and Misunderstandings About Gift Tax in Thailand

Gift tax in Thailand is widely misunderstood, particularly among expats who rely on informal advice from forums or social media. The following points address some of the most common misconceptions.

‘Gift tax does not exist in Thailand’

Gift tax does exist in Thailand and has been part of the tax system since 2016. However, it applies only in specific circumstances and mainly affects large, deliberate transfers of wealth.

The fact that many people never encounter it does not mean it does not apply.

‘Money sent to a spouse is always tax-free’

Transfers between spouses benefit from a higher annual threshold, but they are not automatically exempt.

Regular support for household expenses is usually not treated as a gift. Larger lump sums that are retained or invested may fall within the gift tax framework once thresholds are exceeded.

‘Overseas gifts are never taxed in Thailand’

The location of the giver does not, by itself, determine whether gift tax applies.

If a Thai tax resident receives a large gift that exceeds the relevant threshold, it may be subject to assessment under Thailand’s gift tax rules, even if the funds originate from overseas.

‘Banks automatically report gifts to the Revenue Department’

Banks may ask questions about large transfers for anti-money laundering purposes, but this is not the same as reporting gift tax.

Tax obligations arise from how transfers are classified and declared, not from bank enquiries alone. Consistent explanations and clear records are what matter in practice.

‘If no tax was paid abroad, Thailand cannot tax it’

Different countries tax gifts in different ways. Some focus on the giver, others on the recipient.

The absence of tax in another country does not automatically mean no tax exposure exists in Thailand. Each jurisdiction applies its own rules.

‘Gift tax is never enforced’

Gift tax is not aggressively policed in everyday family situations, but it is part of the law and can become relevant where transfers are large, unclear, or poorly documented.

The real risk is not enforcement for ordinary support payments, but confusion created by poorly structured transfers.

Practical Perspective

Most gift tax issues arise from misunderstanding rather than non-compliance.

Clear intent, sensible structuring, and basic record-keeping resolve the majority of concerns long before tax becomes an issue.

Future Outlook and Regulatory Direction

Thailand’s approach to gift tax is evolving gradually rather than through sudden reform. While the core framework has remained stable since its introduction, broader trends in tax administration and financial regulation continue to shape how gift tax is viewed and applied in practice.

Greater Transparency and Information Sharing

Thailand, like many countries, has moved towards greater financial transparency. This includes closer alignment with international standards on information exchange, anti-money laundering controls, and cross-border reporting.

While gift tax itself has not been fundamentally reworked, large transfers of funds are now more visible to financial institutions. This does not mean gift tax is being newly enforced, but it does mean that clarity of purpose and documentation are increasingly important.

Focus on Substance Over Form

A consistent direction in Thai tax administration is an emphasis on substance over labels.

Transfers described as gifts may still be reviewed based on how the money or asset is actually used. This reinforces the importance of avoiding artificial structures and ensuring that documentation reflects reality.

Trusts and Estate Planning Developments

There has been ongoing discussion around formalising the use of trusts in Thailand. While trusts are not yet a mainstream estate planning tool under Thai law, future developments could influence how lifetime gifts and succession planning are structured.

For expats, this highlights the need to keep gift planning aligned with wider estate and succession considerations, rather than viewing gift tax in isolation.

What This Means for Expats

For most expats, the direction of travel does not signal increased risk in everyday family support or routine financial arrangements.

Instead, it reinforces a simple principle: large or unusual transfers should be planned, explained, and documented, particularly when multiple countries are involved.

Staying informed and periodically reviewing arrangements are usually sufficient to remain compliant as the regulatory environment continues to mature.

Gift Tax: Key Takeaways

- Gift tax exists in Thailand, but it applies mainly to large, deliberate transfers of wealth, not everyday family support.

- Most expats will never pay gift tax, as routine living expenses and household support are usually outside its scope.

- Gift tax is assessed on the recipient, based on the total value of gifts received in a calendar year.

- Higher tax-free thresholds apply to gifts between spouses, parents, and children.

- Large lump-sum transfers, particularly those that are retained or invested, require more careful consideration.

- A gift is not treated as genuine if the giver continues to benefit from it, which is known as a gift with reservation.

- Gift tax is declared through the normal personal income tax return, not a separate filing process.

- Clear documentation and consistent explanations are usually more important than the headline tax rate itself.

- Cross-border gifts require coordination between Thai rules and the laws of other countries involved.

For most expats, understanding the distinction between support and gifts, and keeping sensible records, is enough to manage gift tax risk confidently.

Need Help Understanding How Gift Tax Applies to You?

Gift tax issues are rarely about a single rule. They usually depend on how transfers are structured, documented, and used in practice, particularly where family members or assets are spread across more than one country.

If you would like help understanding how the gift tax rules apply to your situation, or if you want to sense-check a planned transfer before moving money, you are welcome to speak with our team. We can help you clarify where the boundaries lie and how to manage larger transfers with confidence and compliance.

Book a call with the team to talk through your situation and get clear, practical guidance on your next steps.

Frequently Asked Questions

Gift Tax

No. Most expats never pay gift tax because routine family support and smaller transfers fall below the thresholds. Gift tax usually becomes relevant only for large, intentional transfers of assets or cash.

A gift with reservation is where something is described as a gift, but the giver continues to benefit from it. In such cases, the transfer may not be treated as a genuine gift for tax purposes.

Gift tax is declared as part of the annual personal income tax return using form PND.90. There is no separate gift tax filing process.

Banks may ask questions about large transfers for anti-money laundering purposes, but this is separate from tax reporting. Gift tax obligations arise from how transfers are classified and declared on the tax return.

In Thailand, gift tax is assessed on the recipient, not the giver. This is different from some other countries, which tax gifts at the level of the person making the gift.

They can be. The location of the giver does not determine tax treatment. If a Thai tax resident receives a genuine gift that exceeds the relevant threshold, it may need to be assessed under Thailand’s gift tax rules, even if the money comes from overseas.

Not usually. Regular transfers to cover household or living expenses are generally not treated as taxable gifts. Larger lump-sum transfers that are retained or invested may fall within the gift tax rules if annual thresholds are exceeded.

Yes. Thailand has a gift tax that applies when the value of gifts received by an individual exceeds certain annual thresholds. It mainly affects large, deliberate transfers of wealth rather than everyday family support.